PAWNBROKER

We offer pawnbroker loans against jewellery, luxury watches, gold and diamonds,.

Our highly-trained specialists bring a wealth of knowledge and experience in assessing the value of your assets.

Call us or visit our shop in Ashton.

Loan Benefits

QUICK ESTIMATES: Our in-house valuers provide you with quick and accurate estimates on your asset value so we can make you a loan offer

FAST FUNDING: Loan proceeds can be deposited to your account within minutes after you accept your loan offer. We can even pay cash in some circumstances if you are in one of our stores

NO CREDIT CHECKS: We do not perform credit checks and we do not report anything to credit agencies since the loan is secured against your asset

SAFE & SECURE: Your assets are always secure and protected . We insure all assets in our highly secure vaults

FCA Regulated We are regulated by the Financial Conduct Authority

Get Your Assets to Us

Bring your assets to us: Your time is as valuable as your assets. So make an appointment and one of our expert appraisers will be ready to meet & greet and appraise your assets as soon as you arrive.

How Pawnbroking Works

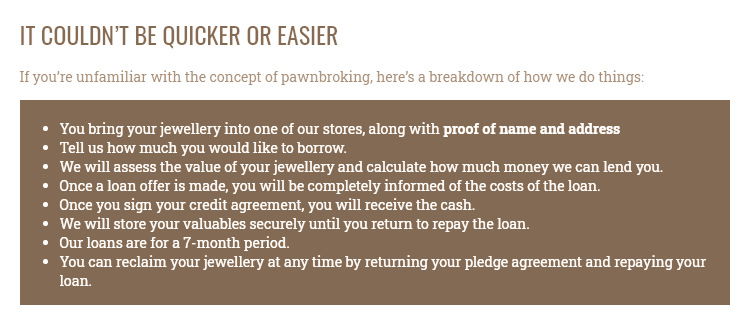

Like a bank a pawnbroker earns income on the interest that is charged on the loan secured by a pledged item. In order to accept goods into pawn a pawnbroker makes an on-the-spot valuation of the goods. The customer and the pawnbroker will agree the sum to be advanced and the pawnbroker presents new customers or indeed existing customers who ask for it, a completed document called 'Pre Contract Information'.

A pawnbroker will lend from as little as £5 to many thousands of pounds in one easy, quick transaction that requires no credit checks or lengthy meetings or form filling.

If the customer wishes to go ahead with the transaction they sign the actual agreement which is an A4 document with details of their rights and protection under the Consumer Credit Act 1974 and the terms and conditions of the loan. The customer also receives as part of the document itself a pawn-receipt for presentation when redeeming the goods. The agreement is usually for a period of six or seven months.

A customer has the right to give notice to withdraw from the agreement within 14 days and also to make partial or full early repayments. They are also entitled to redeem property by payment of the original loan plus the amount due at any time during the contract period.

Unlike other forms of credit, pawnbrokers can assess creditworthiness based on the value of the item if sold. Therefore customers are normally not CRA or credit checked.

When the loan and the interest are paid, the goods are returned to the customer. If the customer has not repaid the loan during this time and the loan was over £100 he will receive notice that the property is due to be sold giving him a further statutory period of 14 days in which to redeem (the customer will normally however have the option at the end of the contract to renew the loan by the payment of interest only and the rewriting of a fresh agreement).

If the customer does not renew or respond to the notice served, the pawnbroker may take steps to dispose of the goods. Having served the notice of his intention to sell the goods the pawnbroker must obtain the true market value on the date of sale which ensures a fair price is obtained for the customer.

Where the proceeds of sale are greater than the amount due to the pawnbroker, the balance is due back to the customer. Unless a full credit check has been undertaken, which is unlikley, the customer is not chased for any debt and will never pay more than the value achieved when the item is sold.

Contrary to popular myth, only where the loan was for less than £75 (and contract period six months) does the pawnbroker gain title to the goods where the customer has not repaid the loan. Again, contrary to what people may believe, the pawnbroker does not wish to gain title to property as he is in the business of lending money and he wishes far more to see the loan repaid without needing to resort to the sale of property. This way not only is the debt cleared in full but the customer is happy at the return of his goods and he has possession of them to return again at some stage in the future. This is proved by the very high volume of trade that is repeat transactions - nearly always with the same security and very often several times in a few months.

If you were to walk into a pawnbroker's shop today you could be forgiven for thinking that you had just walked into your local bank or building society. Pawnbroking is now a serious alternative to using the services provided by the High Street bank. Customers realise that borrowing money against goods they already own is an affordable alternative to a bank overdraft or other type of loan.

Pawnbroking businesses are on the High Street and are very often jewellery retailers giving them a perfect shop set-up for lending and for keeping goods safely in storage. Consequently, the security that the vast majority of pawnbrokers give loans against is gold, jewellery and watches. This is because they are:

- easy to value

- easy to store

- are a luxury 'can do without' item

- do not perish

- do not generally depreciate

- have an established second-hand market

A pawnbroker will lend from as little as £75 to many thousands of pounds in one easy, quick transaction that requires no credit checks or lengthy meetings or form filling. Short-term cashflow is the reason most people use a pawnbroker, where convenience and speed of service are quite unrivaled. A loan will just as often be obtained for some extra spending money as it will be to clear an outstanding telephone bill. It is flexible, transparent, competitively priced and immediate and it is these factors that customers prefer. The result is that a high number of customers are satisfied with the service they receive.